Carbon Accounting Essentials: Charting a Path to Environmental Responsibility and Financial Resilience

The urgent need to transition to a low-carbon economy has spurred various market measures aimed at tackling the looming threat of climate change. While the scientific aspect of climate mitigation and adaptation remains crucial, understanding the economics of climate change is equally vital. The rise of market measures such as green bonds and sustainability-linked bonds and the increasing emphasis on Environmental, Social, and Governance (ESG) criteria underscore the significance of corporations disclosing metrics and targets to users of financial information. Consequently, measuring carbon emissions associated with organizations’ operations and activities becomes paramount to participate in the carbon market.

The urgent need to transition to a low-carbon economy has spurred various market measures aimed at tackling the looming threat of climate change. While the scientific aspect of climate mitigation and adaptation remains crucial, understanding the economics of climate change is equally vital. The rise of market measures such as green bonds and sustainability-linked bonds and the increasing emphasis on Environmental, Social, and Governance (ESG) criteria underscore the significance of corporations disclosing metrics and targets to users of financial information. Consequently, measuring carbon emissions associated with organizations’ operations and activities becomes paramount to participate in the carbon market.

Greenhouse gas emissions (GHGs) have been identified as major contributors to climate change. These gases, emitted from various sources, exert a radiative forcing effect, influencing changes in climatic systems. The pursuit of economic growth drives the utilization of primary energy resources, which generate emissions either directly or indirectly. The Greenhouse Gas Protocol offers a comprehensive standard for computing greenhouse gas accounting, encompassing the GHGs listed in the Kyoto Protocol. While carbon accounting primarily focuses on carbon dioxide, the most prevalent greenhouse gas, it also encompasses other emissions.

Source: Corporate Finance Institute

Carbon accounting stands at the intersection of environmental and financial management, pivotal in addressing climate change and promoting sustainable business practices. It revolutionizes how organizations measure, report, and manage carbon emissions, reflecting a broader commitment to environmental stewardship and social responsibility. Carbon accounting is a technique employed to gauge the extent of an organization’s carbon emissions, both direct and indirect.

Various factors, including the determinants of carbon markets, the advent of green bonds, and reporting standards, shape the evolution of carbon accounting and reporting. Works by Bebbington and Larrínaga shed light on carbon trading and accounting complexities, highlighting the importance of understanding the financial and accounting facets for accurate and transparent reporting.

The emergence of carbon trading markets has raised pertinent financial accounting questions, particularly regarding recording carbon credit in financial books. This underscores the need for robust accounting practices to capture and report carbon-related financial transactions faithfully. Quantifying international public finance for climate change adaptation has become pivotal in grasping the economic implications of climate change. Studies by Zhang et al. emphasize the significance of considering carbon trading prices in the cost accounting of environmental systems, accentuating the financial and economic dimensions of carbon accounting and its broader impact on sustainability.

The advent of carbon accounting has deepened our understanding of the economic ramifications of carbon emissions and the potential for carbon pricing mechanisms to drive sustainable development. The discourse on carbon accounting underscores the interconnectedness of environmental and financial considerations, underscoring the need for comprehensive reporting frameworks to guide sustainable business practices. As organizations grapple with the impacts of climate change, the focus on carbon accounting remains integral to efforts to enhance resilience and foster sustainable development.

While various frameworks exist for accounting for emissions, including the GHG Protocol, the Partnership for Carbon Accounting Financials, and ISO 14040, they provide robust frameworks for emissions accounting. As organizations embark on their decarbonization journey, computing emissions becomes critical to track performance.

Carbon accounting facilitates market transparency and price discovery in carbon markets, aiding investors and businesses in making informed decisions. It enables access to climate finance by providing reliable data on emissions and supporting the funding of emission reduction projects. Additionally, carbon accounting incentivizes innovation and risk management, driving the transition to a low-carbon economy.

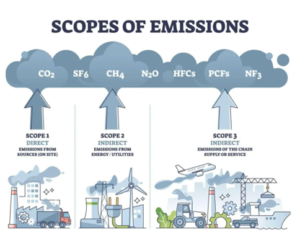

In Nigeria, the Climate Change Act and the adoption of the International Financial Reporting Standards (IFRS) impose a responsibility on organizations to determine their emissions and devise emission reduction plans aligned with the Nationally Determined Contributions (NDC). Thus, the journey to determine emissions necessitates introspection and a deeper examination of the supply chain to account for Scope 3 emissions.

While challenges exist with carbon accounting, such as the need for assumptions and the risk of double counting or under-reporting, the focus should remain on identifying emission sources and mapping out a decarbonization pathway. Furthermore, the complexity of measuring emissions accurately across diverse sources, navigating regulatory frameworks, and addressing uncertainties related to emission factors and carbon offsetting pose significant challenges for organizations implementing carbon accounting practices.

In conclusion, the emergence of carbon accounting has transformed how organizations approach environmental and financial management, reflecting a broader commitment to sustainability and social responsibility. The evolving trends in carbon accounting underscore the importance of robust accounting practices and financial considerations in addressing climate change and promoting sustainable business practices. As the field of carbon accounting continues to evolve, it is expected to play a pivotal role in driving positive environmental and financial impacts while delivering long-term value to organizations and society.